The 70% Fixed Cost Trap: How to Survive a Top-Heavy Budget When Rent or Mortgage Eats Your Paycheck

- My PenPoint Team

- 2 days ago

- 7 min read

You open your banking app on payday and, for a few hours, you feel almost wealthy. Then rent clears. The mortgage auto-payment goes through. Insurance, the car note, the minimum on your loan.

By the next morning, most of your paycheck is already gone - and you haven't bought a single grocery yet.

If that sounds familiar, you're not bad with money. You're stuck in what's called a top-heavy budget: one where your fixed costs are so large that no amount of skipping lattes will fix it. This is the 70% fixed cost trap, and escaping it requires a different playbook than the usual "just spend less" advice.

This guide breaks down exactly what the trap is, how to know if you're in it, and the practical steps to survive — and eventually escape — a budget where housing eats far more than it should.

What is the 70% fixed cost trap?

The 70% fixed cost trap is a situation where your unavoidable, recurring bills — rent or mortgage, utilities, insurance, loan payments, transportation — consume roughly 70% or more of your take-home pay. That leaves only about 30% to cover food, savings, debt payoff, and everything else life throws at you.

The problem isn't just that money is tight. It's structural. When fixed costs are this high, the flexible part of your budget is too small to absorb a shock. One car repair, one medical bill, or one slow month at work and you're forced onto a credit card. You're not overspending — you're over-committed.

Financial planners often point to the 50/30/20 rule, popularized by U.S. Senator Elizabeth Warren, as a healthy baseline: about 50% of after-tax income for needs, 30% for wants, and 20% for savings and debt. A top-heavy budget flips this on its head. Needs alone swallow 70%, wants and savings fight over the scraps, and the math simply doesn't balance.

Fixed costs vs. variable costs: know what you're fighting

Before you can fix a top-heavy budget, you have to sort your spending into two buckets, because each one requires a completely different strategy.

Fixed costs are the large, predictable payments that stay roughly the same each month and are hard to change quickly:

Rent or mortgage

Property taxes and homeowners/renters insurance

Car payments and auto insurance

Loan and minimum debt payments

Childcare or tuition

Core utilities and internet

Variable costs are the smaller, flexible expenses you have real control over week to week:

Groceries and dining out

Subscriptions and entertainment

Clothing and shopping

Rideshare, fuel, and discretionary transport

Hobbies and impulse buys

Here's the uncomfortable truth: most budgeting advice targets variable costs because they're easy to cut. But in a top-heavy budget, the variable bucket is already small. Trimming a $6 coffee habit feels productive, but it won't rescue you when 70% of your income is locked into fixed obligations. The real leverage — and the real difficulty — is in the fixed bucket.

Why 30% is the benchmark (and why 70% is dangerous)

For decades, the widely accepted rule of thumb has been that housing should cost no more than 30% of your income. Spend more than that, and government and academic researchers formally classify you as "cost-burdened." Spend more than 50% on housing alone, and you're "severely cost-burdened."

This isn't a fringe problem anymore.

According to Harvard's Joint Center for Housing Studies State of the Nation's Housing 2025 report, half of all U.S. renters — a record 22.7 million households — were cost-burdened in 2023, and roughly 27% were severely cost-burdened, spending more than half their income on housing. Among homeowners, about 24% were cost-burdened as well, driven up by rising insurance premiums and property taxes rather than the mortgage alone.

Even the middle class is feeling it. The same body of research shows the cost-burden rate for renters earning $45,000 to $74,999 has roughly doubled since 2001. In other words, the top-heavy budget is no longer just a low-income problem — it's a mainstream one.

The danger of crossing into that 70% zone is what economists call low residual income: the money left after housing to cover food, medicine, transport, and emergencies. When that cushion disappears, ordinary life becomes a series of near-misses, and any surprise turns into debt.

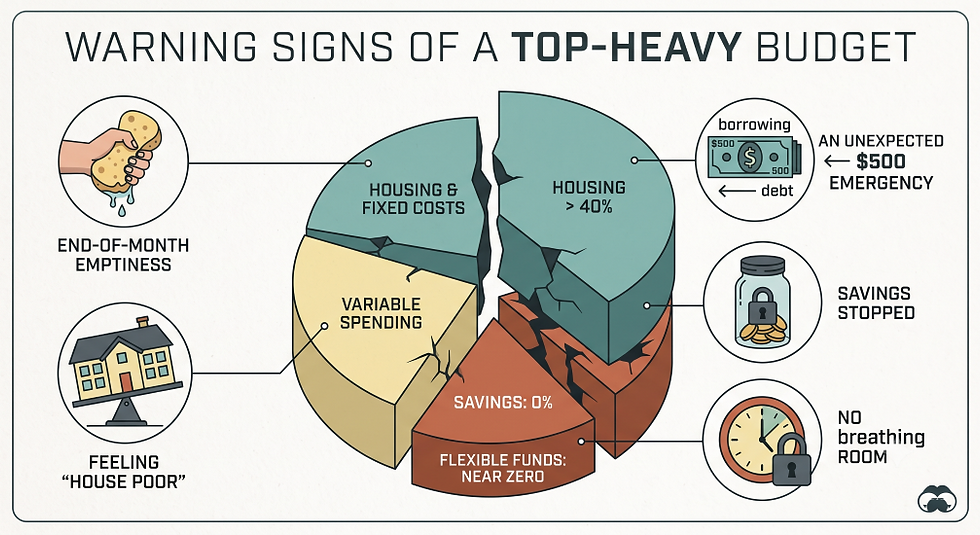

Signs you're stuck in a top-heavy budget

You may be in the fixed cost trap if:

Your rent or mortgage alone is more than 35–40% of your take-home pay.

You reach the end of the month with little or nothing left, even when you "behave."

An unexpected $500 expense would force you to borrow.

You've stopped saving entirely because there's simply no room.

You feel "house poor" — you have a nice place to live but no financial breathing room.

If two or more of these ring true, the good news is that recognizing the pattern is the first real step. The next steps are about buying back your breathing room.

How to survive a top-heavy budget: a step-by-step plan

1. Rebuild your budget around reality, not a rule

The standard 50/30/20 split assumes housing fits inside a 50% "needs" bucket. Yours doesn't — so stop measuring yourself against a rule you can't currently meet. Instead, assign every single dollar a job based on your actual numbers.

Start by listing your true monthly essentials, then everything else. This zero-based approach shows you precisely how much flexibility you really have. If you've never done this or your categories feel broken, our walkthrough on how to fix your budget when you're always running out of money gives you a realistic framework to start from.

2. Win the quick battles in your variable spending

Yes, variable costs won't save you alone — but in a crisis, quick wins buy time and momentum. Audit your subscriptions, pause anything you haven't used in 30 days, and pick one recurring discretionary expense to cut rather than trying to eliminate everything at once. The goal is to free up cash flow fast while you work on the bigger, slower fixes.

If you're running a household on a single paycheck, the pressure here is even higher. These smart budgeting tips for families living on one income show how to stretch limited variable spending without feeling deprived.

3. Attack the fixed costs — this is where the real money is

This is the hard part most advice skips, so tackle it directly:

Housing: Consider a roommate, renting out a spare room, or negotiating your lease renewal instead of accepting an automatic increase. If you own, explore whether refinancing or appealing your property-tax assessment could lower the payment.

Insurance: Re-shop your auto, home, and renters policies once a year. Bundling or raising a deductible can cut premiums meaningfully.

Debt: Look into consolidating high-interest balances into a lower fixed payment so more of each dollar goes to principal.

Transportation: A car payment is a fixed cost in disguise. Downsizing to a cheaper vehicle can free up hundreds a month.

You won't win all of these. But even one successful renegotiation on a fixed cost is worth more than months of skipped coffees.

4. Grow the top line, because cutting has a floor

Here's the math nobody likes: you can only cut expenses down to zero, but you can grow income without a ceiling. Once you've trimmed what you reasonably can, the fastest path out of a top-heavy budget is usually earning more.

That might mean a raise, a side hustle, freelancing, or moving into higher-paying remote work. If a location-independent income appeals to you, our complete guide to remote work in 2026 breaks down the most in-demand, best-paying remote skills worth building this year. Even an extra few hundred dollars a month, directed entirely at your fixed obligations, can change the shape of your whole budget.

5. Build a micro-buffer before anything else

When you're this stretched, a full three-to-six-month emergency fund feels impossible — so don't aim for it yet. As the Consumer Financial Protection Bureau notes, even a small amount set aside can provide real financial security. Aim for a starter buffer of $500 to $1,000. That small cushion is what stops the next surprise from turning into credit card debt, which is what keeps top-heavy budgets top-heavy.

Start tiny and automate it. Our step-by-step guide on how to build an emergency fund even on a low income shows how small, consistent contributions add up faster than you'd expect.

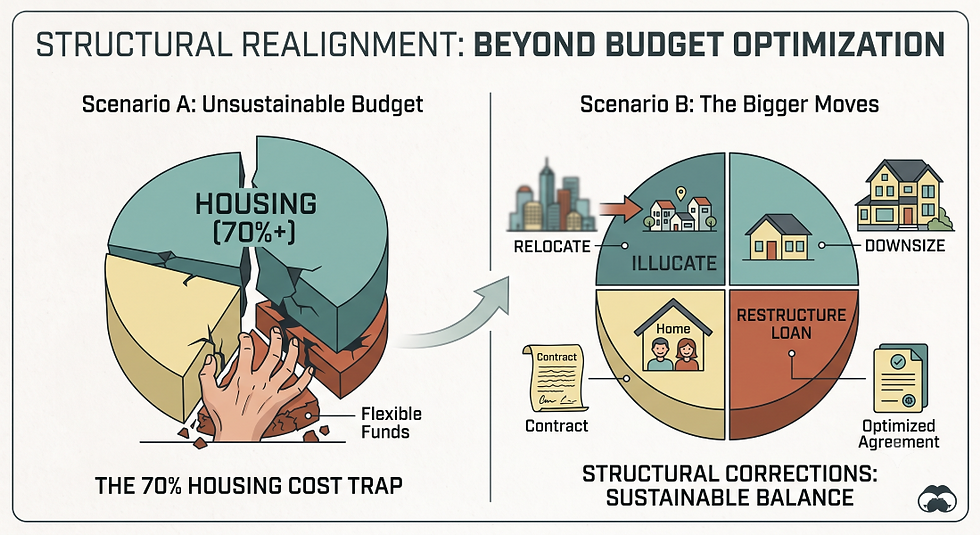

6. Know when the answer is a bigger move

Sometimes the numbers simply don't work, and no amount of optimizing a 70% housing cost will fix them. That's not failure: it's information.

If your fixed costs are structurally too high for your income, the highest-impact decision may be a bigger one: relocating to a lower-cost area, moving to a smaller place, taking on a housemate, or restructuring a loan. A budget you can actually sustain beats a prestigious address you can't.

Frequently asked questions

What does it mean to have a "top-heavy" budget?

A top-heavy budget is one where fixed, unavoidable costs — especially housing — make up the majority of your income, leaving little flexibility for savings, emergencies, or discretionary spending. It's "top-heavy" because the biggest, hardest-to-change expenses dominate everything else.

How much of my income should go to rent or mortgage?

The traditional benchmark is no more than 30% of your income on housing. Beyond that, you're considered cost-burdened; beyond 50%, severely cost-burdened. In today's market many people exceed this, but the closer you can get to 30%, the more financial breathing room you'll have.

What does "house poor" mean?

Being house poor means you spend such a large share of your income on your home that you have little left for other goals — you have a nice place to live but no financial cushion. It's a common symptom of the fixed cost trap.

Should I cut small expenses or big ones first?

Cut a few small variable expenses immediately for quick wins and cash flow, but understand that lasting relief comes from lowering your large fixed costs or raising your income. Small cuts buy time; big moves buy freedom.

Can I get out of the trap without moving?

Often, yes — through renegotiating rent, re-shopping insurance, consolidating debt, adding a housemate, and increasing income. But if housing is structurally unaffordable for your earnings, relocating or downsizing may be the most powerful single fix available.

The bottom line

A top-heavy budget isn't a character flaw — it's a math problem. When 70% of your paycheck is spoken for before you buy a single meal, willpower and coupon-clipping were never going to be enough. The way out is to stop fighting only the small, easy expenses and start working on the big levers: your fixed costs and your income. Do that consistently, protect yourself with even a small buffer, and you slowly turn a budget that controls you into one you control.

Start with one step this week. Momentum, not perfection, is what gets you out of the trap.

This article is for general informational and educational purposes only and does not constitute financial advice. Everyone's situation is different; consider consulting a qualified financial professional before making major money decisions.

Want more where this came from? Follow My PenPoint and never miss a guide that helps you keep more of your paycheck and stress less about money.

Comments